Table of Contents

Recent legislative and regulatory changes have introduced new compliance requirements for clean energy tax credits in the United States. Projects claiming incentives under Sections 45X, 45Y, and 48E must now consider whether components or supply chains involve Prohibited Foreign Entities (PFEs).

These requirements stem from amendments introduced under the One Big Beautiful Bill Act (OBBBA), enacted July 4, 2025, and subsequent implementation guidance from the Internal Revenue Service (IRS Notice 2026-15).

and subsequent implementation guidance from the Internal Revenue Service (IRS Notice 2026-15).

For developers, EPCs, and organizations planning projects beginning construction in 2026 or later, understanding the Material Assistance Cost Ratio (MACR) framework and associated compliance requirements has become a critical part of project planning.

This article explains what changed, how the Material Assistance Cost Ratio (MACR) works, and what project owners should be doing now for 2026 and beyond.

Legislative Background

Federal clean energy incentives were significantly expanded through the Inflation Reduction Act (IRA) of 2022, which established several long-term tax incentives designed to accelerate renewable energy deployment and domestic manufacturing.

Key provisions include:

- Section 45X – Advanced Manufacturing Production Credit

- Section 45Y – Clean Electricity Production Credit

- Section 48E – Clean Electricity Investment Credit

These incentives were created to support the domestic clean energy economy while encouraging supply-chain development within the United States.

However, the One Big Beautiful Bill Act (OBBBA) introduced additional safeguards related to foreign influence in critical supply chains. These safeguards created Prohibited Foreign Entity restrictions that can affect eligibility for the above credits.

In February 2026, the IRS released Notice 2026-15, providing interim guidance on how to interpret these restrictions and how taxpayers should calculate compliance metrics such as the Material Assistance Cost Ratio.

Sources

- U.S. Congress – Inflation Reduction Act of 2022

- One Big Beautiful Bill Act (OBBBA), enacted July 4, 2025

- Internal Revenue Service – Notice 2026-15 Interim Guidance

What Is a Prohibited Foreign Entity?

A Prohibited Foreign Entity (PFE) falls into one of two categories.

1. Specified Foreign Entities (SFEs)

These are entities explicitly identified by the U.S. government, including:

- Companies on national security or sanctions lists

- Certain Chinese military-linked companies

- Foreign government-controlled entities from China, Russia, Iran, or North Korea

If material assistance comes from one of these entities, the credit is automatically at risk.

2. Foreign-Influenced Entities

More subtle and more dangerous. A U.S. or other company that isn’t on a list but has significant ties to the SFE on the left here. You’re foreign-influenced if a sanctioned foreign entity:

A company may become foreign-influenced if a sanctioned or covered-nation entity:

- Owns 25% or more (or 40% aggregate) of the company

- Holds 15% or more of its debt

- Has the right to appoint executives or board members

- Exercises effective control over production, facilities, or IP

Key takeaway: A supplier does not need to be foreign-owned to create PFE exposure.

Understanding the Material Assistance Cost Ratio (MACR)

The Material Assistance Cost Ratio (MACR) is the primary compliance metric introduced in IRS guidance.

MACR = (Total Direct Costs – PFE Direct Costs) / Total Direct Costs expressed as %

MACR determines whether a facility or component received too much value from PFEs.

In simple terms:

MACR compares the cost of manufactured products and components sourced from non-PFE suppliers against total manufactured product costs.

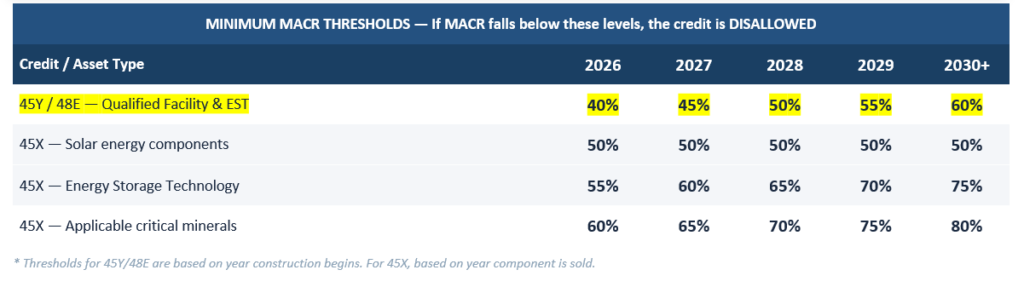

Each year, projects must meet a minimum MACR threshold.

If the ratio falls below that threshold, the entire credit is disallowed.

For example:

- A 2026 solar facility must source at least 40% of manufactured product costs from non-PFE sources

- The required percentage increases in later years

This makes early supply-chain planning critical.

Source

IRS Notice 2026-15 – Interim Safe Harbor Guidance

The Three IRS Interim Safe Harbors

To reduce compliance burden, the IRS introduced three safe harbors. These are optional, but extremely important.

1. Identification Safe Harbor

Helps answer: Which manufactured products and components am I using?

Best for early project scoping, but requires accurate classification. Use the tables from Notices 2023-38, 2024-41 & 2025-08 to identify which Manufactured Products (MPs) and MPCs you are using

2. Cost Percentage Safe Harbor

Helps answer: What did they cost?

Use the Assigned Cost Percentages from IRS tables to compute Total Percentage and Total PFE Percentage. This is often the lowest-risk option for modeling MACR.

3. Certification Safe Harbor

Helps answer: Were these components produced by a PFE?

Relies on signed supplier certifications stating components were not PFE-produced.

⚠️ Important limitation:

Protection is lost if the taxpayer knows or should know the certification is false.

Why Non-Profits Face the Highest Risk

Entities using Section 6417 elective pay face unique exposure.

If a credit is later disallowed due to MACR errors:

- The IRS can claw back direct payments

- Repayment obligations can arise years after construction

- Budget shortfalls can be severe

For non-profits and public entities, supplier certifications and documentation are not optional, they are essential.

Penalties & Compliance Risks

6662(m) — Energy Credit Disallowance Penalty

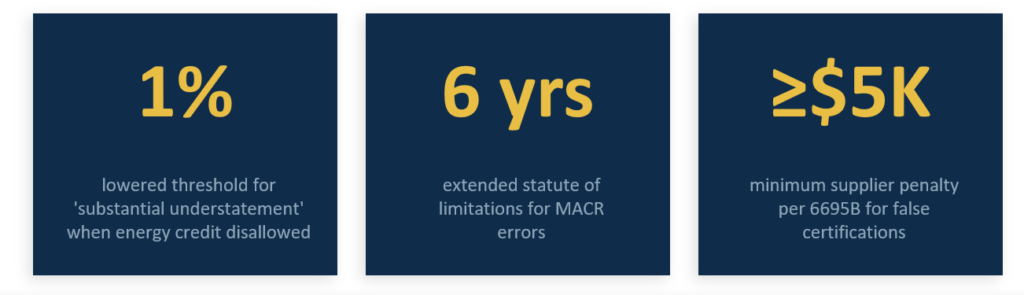

When a credit under 45X, 45Y, or 48E is disallowed due to MACR overstatement, the ‘substantial understatement’ threshold drops from 10% to just 1% of tax — dramatically increasing penalty exposure.

6695B — Supplier Certification Penalty

Suppliers who knowingly provide false PFE certifications face a penalty equal to the GREATER of 10% of the resulting underpayment OR $5,000. Applies to certifications issued after December 31, 2025.

6417 Elective Pay Impact

Tax-exempt and governmental entities that elected to receive direct payments for credits face repayment obligations for excessive payments arising from a MACR-related credit disallowance.

These rules make PFE compliance a top audit priority for the IRS.

What Clean Energy Project Owners Should Do Now

For any project starting construction in 2026 or later, action is required immediately:

✔ Begin supplier and supply-chain audits

✔ Collect and track PFE certifications

✔ Model MACR early — before procurement

✔ Update contracts to require ongoing compliance

✔ Maintain documentation for at least six years

Projects that wait until tax filing are already too late.

Final Thoughts

PFE and MACR rules are now law, not guidance.

They fundamentally change how clean energy projects must source, document, and manage risk.

Early projects still have flexibility but that window is closing fast.

Organizations that act now will protect their credits, their investors, and their long-term viability.

Learn More

Organizations evaluating compliance strategies related to PFE, FEOC, domestic content requirements, and safe harbor frameworks may benefit from reviewing additional technical resources and regulatory guidance as they plan future projects.

Additional materials and technical briefings on these topics are periodically shared by industry organizations and compliance advisors working across the renewable energy sector.

IMPORTANT DISCLAIMER

This article is provided for informational and educational purposes only. It does not constitute legal, tax, or regulatory advice.

Energy credit eligibility, supply-chain compliance requirements, and tax credit calculations may vary based on project structure, ownership, and regulatory interpretation.

Readers should consult qualified tax advisors, legal counsel, or regulatory professionals before making decisions related to energy tax credits or supply-chain compliance.

References to legislation or regulatory guidance are based on publicly available sources at the time of publication.

Sources: This article references publicly available legislative and regulatory materials including the Inflation Reduction Act of 2022 (Public Law 117-169) and its clean energy tax credit provisions under Internal Revenue Code Sections 45X, 45Y, and 48E, amendments introduced under the One Big Beautiful Bill Act (OBBBA), enacted July 4, 2025, and implementation guidance issued by the Internal Revenue Service in Notice 2026-15 relating to Prohibited Foreign Entity (PFE) restrictions and Material Assistance Cost Ratio (MACR) calculations. Additional references include relevant sections of the U.S. Internal Revenue Code such as Section 6417 (Elective Pay/Direct Pay), Section 6662 (Accuracy-Related Penalties), and Section 6695B (Penalties for False Energy Credit Certifications), along with national security and foreign-entity definitions referenced in federal statutes including provisions of the National Defense Authorization Act (NDAA) and publicly available listings from U.S. government agencies related to entities of concern. Authoritative information is drawn from official government sources including U.S. Congress (congress.gov), the Internal Revenue Service (irs.gov), the U.S. Department of the Treasury (treasury.gov), and the Legal Information Institute at Cornell Law School (law.cornell.edu).

Want deeper guidance?

Contact our team to discuss supply-chain readiness for your 2026 projects.

About Energy Solutions and Supplies (ESAS)

At ESAS, we bring together products, logistics, and professional expertise to ensure your solar + storage projects are built to last. Whether you’re navigating project design, procurement, or execution, our team is here to support your growth in 2026 and beyond.

👉Need a feasibility check or shading analysis for your next C&I project?

Our Professional Services team can support from concept to completion.

Contact ESAS today.

Get in touch with one of our representives

Stay Connected with ESAS

Energy Solutions and Supplies LLC

Phone: +1 480-478-1616

Website: www.energysolutions-solar.com

Latest Events and Updates:

Our Events | Trade Events

Stay connected with us on

LinkedIn, Facebook, Instagram, and YouTube for the latest updates.